The issue of most major banks until today is that they follow a strategy of a very deep and a very wide value chain. That means, they offer a huge variety of products, which they handle from IT to after sales support. And everything in between. They run the core banking infrastructure, pre sales, the core product, and after sales.

The products range from retail banking, private banking & wealth management, products for external asset managers like tax advice and private label funds, to internal asset management and investment strategy and research products. Further, most banks offer corporate banking (split between SMEs and large caps), treasury, FX, brokerage, leasing & factoring, global finance and transaction banking, transportation, fixed income, equity and M&A. In addition, retail banking, credit, mortgages, all kinds of saving products, pension products, investment products – and payment. The list could be extended both vertically and horizontally.

In short: banks offer a huge variety of deeply integrated products.

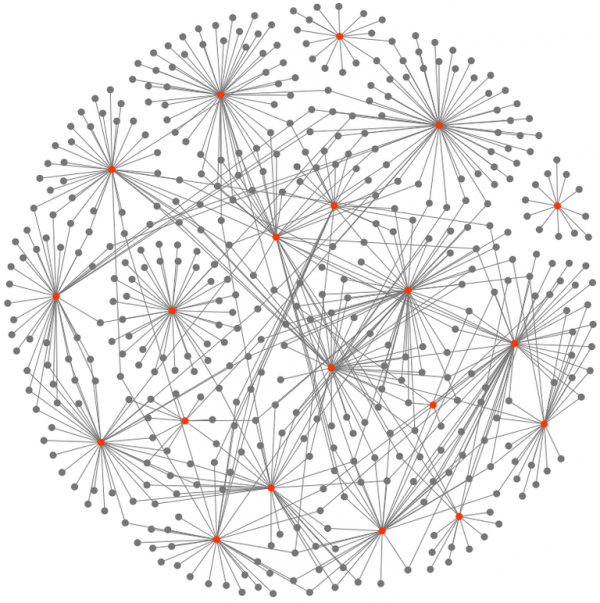

This makes it is easy to cut of some edges and start a highly specialized business. This is what we see every week now. We call them FinTech startups.

Not only is it easy to leave out some services that banks still run in-house (scoring, KYC, IT) around their products. But banks also offer this service in pricy real estate locations. They call them bank branches. Most of us have not set foot in one lately.

This opens a broad flank for highly specialized companies to target one product only. Dissect the offering, add a modern IT infrastructure (cloud, mobile, analytics, prediction, big data, a revamped contract / KYC handling), and sell it cheaper than any account manager in a nice suite could do. Online.

This is what we see in the current FinTech boom.

The width of banks horizontal diversification and the depth of value creation of banks is still archaic. Few industries have managed to cope with this structure as long as banks. Most industries have trimmed down to their core business by now. When you try to do everything, you don’t do anything right. This has lead to the fact that most retail bank product offerings are interchangeable, as no one is really bad, but no one is really good either. That’s where the brand of a bank comes into play to convince customers to go with one or the other offering. And if in addition you have a huge capex underlying, competing on price gets difficult, too. As even most vertically specialized banks still operate a big amount of their vertical activities themselves, there is a big chunk of optimization potential for newcomers in the operations alone. We see this in the competition of classical direct banks with mobile banks for example.

Let’s face it, overall banks today still look and feel like general supply shop from the 80s.

The specialization and disruption which we have seen in other industries (e.g. travel, traditional retail, communications) now accelerates in financial services / banking. Things started to change ten years ago slowly, but the acceleration we see in Europe over the last three years is impressive.

That is not a problem by any means. We have seen this disruptive development in other industries already – where highly specialized players and services have shifted to become complementary partners. Add the degree of digital technologies and user adoption to them, and you can explain what is happening in FinTech today.

We as VCs are happy to see so much disruption in the industry. Not all FinTech startups will be successful, but one thing is sure: some will. And banks will struggle to justify their existing cost structure, and margin business. It will take time to disrupt the industry to the degree that we see others being chopped up and put together again.

However, what we see right now is a race into all verticals of banks.

And it would be beneficial for banks to realize, that this is 2015.