The post I do not want to own that car appeared first on signed.vc.

]]>For the first time in my life I have been spending (way too much) time at new car dealerships in order to get a car. Moved to Sweden. Want to see the nature. Need a car. Simple.

The search started in Germany, but I continued here in Sweden for the last three weeks. I had a simple mission: I have a budget of X that I want to spend per month on mobility. I did not care which car I got, but I wanted to get the best car possible for my monthly budget. I obviously want to maximize the car (Audi A4 being better than A3 or Mercedes E-Class being preferred over C-Class) but was not set on a brand or a particular model. Not an engine or even a color. Of course I had preferences, but ultimately I just wanted to get the best car for my budget.

Sounds like a simple task. With leasing and financing options being marketed everywhere.

Turns out, not so much the case.

On my journey to find a car that fits my monthly budget, I have now visited 17 dealerships in two countries (Mercedes, Audi, BMW, Skoda, Volkswagen, Mazda, Jeep). Yes, I am still on vacation and have time.

We are so used to price filters and option checkboxes and sorting algorithms from buying online, that it felt like the 1990s when not a single car salesman could perform the task: Whats the best car I can get in this dealership for x per month? Available now and not built to order. Without being determined on which model, or which engine, or which navigation system version, or which leather color, they were stuck. So we started with one more or less random model, and the price was either dramatically under, or dramatically over my budget. The search in their antiquated on premise installation plus calculation for lease price usually took 20-30 minutes per car.

By the third car and we were still wildly guessing which car might fit the budget, the salesmen usually commented in the likes of “Yeah, this software really sucks” or “I know, this must be frustrating”.

The fascinating thing: the sticker price of the car has literally no influence on the monthly payment price. A car with the value of 30.000€ could end at a leasing of 500€ (same time, same mileage) or at 1000€. Two cars priced the same – if I wanted to purchase them – often had a factor of 3 price difference on the leasing price. The sales men were as baffled as I was.

The simple fact that I do not want to own the car, but want to spend money on my monthly transportation fascinated most of them. This has been a complicated journey. I doubt that this is because the sales men didn’t now their job. Did I invent a new way of thinking about transportation?

Well it does not seem like it.

So here is my shoutout: would someone please develop a brand overarching SaaS solution which allows customers to search for cars available at dealerships in their region based on monthly budget, and not based on V4 vs V6 or 2.0TDI vs 1.8TFSI?

I will make sure you get funding!

Result after way too much time wasted: I ended up with an ok car (not what I had in mind), but at 50% of my originally set monthly budget. So thats good. I guess.

The whole car purchasing experience feels so antiquated. From front to end.

The post I do not want to own that car appeared first on signed.vc.

]]>The post WTF Berlin appeared first on signed.vc.

]]>What the f is happening in Berlin? I met four companies this week, all of them impressive. The quality of companies over the last four years has been increasing to such a degree, that meetings are so refreshing and thrilling.

1. Berlin knows how to pitch

I wrote it before, and I say it again: the quality of pitches in Berlin has increased significantly. To a degree where I am stunned. It is such a blast to meet with people who so adroitly articulate complicated technologies or give motivational speeches on how to conquer markets. To jointly brainstorm about strengths and weaknesses of certain approaches. This is the part of the job that I enjoy the most. It simply tickles when you meet someone who burns for his idea, and you feel he/she is on to something.

The bar is rising.

Quality of pitches at #techstars Berlin is stunning!

— Simon Schmincke (@simonschmincke) September 10, 2015

2. Berlin is connected to capital like never before

We VCs often like to believe we have proprietary access to deal flow, in our region, in our vertical. That is possible if the other side of the table does not know how reach out to captial. That might have been the case some years ago. Today, with active super angels who have built tight relatioships with the top VCs in Europe and the US, no deal is proprietary any more. Or maybe, I am missing these. But when a 3 founder team in Kreuzberg working from their apartment is already talking to some of the top 5 VCs in Europe a week after launch, you know that access to capital is ubiquitous.

Plus factor in the Americans:

Cheers to Adam for the data.

Cheers to Adam for the data.

And this is great for Berlin. This will change things. The pace will increase. We as VCs need to adopt our processes, we need to make quicker decisions, we need to be on top of things like never before.

I am looking forward to a fast paced 2016.

3. Berlins builds tech

Berlin can do e-commerce. Not that this is bad, but the single-focus-stigma we had some years ago can be dropped in 2016. Berlin builds tech. The mindset of technical founders, founding CTOs, quality of international tech talent and a “tech first focus” that I find in so many companies nowadays has clearly broadened the investment scope for companies in Berlin.

It is great to see some groundbreaking technology built in Berlin.

4. Berlin executes like hell

And yes, we can still execute like few others. When the Movinga guys told me last year some of the top level management had bought camping beds to not waste any time commuting to the office, I knew we would at least not be out executed. Cheers to Index for agreeing. Combine this with access to capital, and the technological foundations, and I am most certain we will make an even bigger dent on the European landscape.

5. Berlin is buzzing

7 investment funds to be closed this year in Berlin. Some few hundred million € raised with Berlin focus in the last 12 months. Funds like us who appoint dedicated Berlin fund managers and put both focus and money on the city. Professionalized founding processes. Lawyers who understand founder friendly contracts and know how to benchmark them internationally. Rent’s still ok. Food still amazing. Non-German-Speaking founders moving to the city to build their next company.

I have one prediction for the end of 2016. When we look back on this year in the Startup and Venture scene in the city, we will simply say: WTF Berlin!

The post WTF Berlin appeared first on signed.vc.

]]>The post Thank you and goodbye Earlybird appeared first on signed.vc.

]]>

After two crazy years I had built three companies for Rocket Internet literally around the globe. It was clear that I did not want to do another sprint to build up a company and then leave it – which was the model I was employed for at Rocket. And I wanted to go back to Europe.

WTF is a VC?

Just before I left New York, I sat with Rainer Merkle from Holtzbrinck Ventures at a small burger joint in the West Village for a good two hours. He was the first one who explained to me what he was doing as a VC. At least he tried: Meeting the brightest people who work on the edge of innovation. Literally on issues and technologies that push boundaries and society step by step.

I had no idea what he was really doing. It sounded awesome. That’s what I wanted to do.

It was Alexander Kudlich and Matthias Müller from Rocket who wrote the first introduction to Ciaran O’Leary, who later became my mentor at Earlybird.

My first job interview with a VC happened while I was sharing a falafel plate at a place called Yarock on Torstraße in Berlin with Ciaran. I thought it was odd but down to earth at the same time. It became a place where I had many more falafel in the coming years. These guys seemed to be great to hang out with.

It took Earlybird a good two months and eight interviews in two cities to make up their mind. They had told me to come by the office to give me feedback on my last chat. I stumbled into the 5th floor office in Berlin Mitte, it was 30 degrees and raining heavily outside. I was soaked. Jason opened the door not to tell me if I mad the cut or not, but to have another interview. I hardly remembered any of my answers when I left a good 60 minutes later, yet sure that I had just screwed up.

Still no clue!

Three days later Ciaran called me and told me they wanted me on board. I was very nervous and excited at the same time. I started working with Max Claussen, Christian Nagel and Ciaran in the Berlin office, Hendrik Brandis and Jason Whitmire in Munich. I had never built a cap table, designed a term sheet or read a full investment agreement. I knew hardly any VCs or what to do first. Nevertheless these guys gave me one of their three meter desks in the Berlin office. Boy was I nervous, my learning curve was more than steep. Christian and Ciaran simply threw me into meetings and events. I had to catch up quick. I was not sure if I ever had the chance to survive in this job.

I remember a private equity event in Frankfurt where I had to represent Earlybird and explain the current fund strategy in front of roughly 200 bankers on stage. I was maybe 8 weeks into the job. I don’t think I have ever been so scared, I actually considered not getting up on stage when they called my name.

This was one of many examples where the folks at Earlybird simply trusted me. They let me do. I am sure the mistakes I made where countless, but nevertheless they let me take on responsibility, termsheet negotiations, board seats and work with our portfolio companies quicker than I had imagined. I considered myself more than lucky. After two and a half years I was chairman of the board for a 100m$ company and the current star in the Berlin Startup scene. Not because I was the smartest guy in the Earlybird office, but because the guys put trust in me. I really appreciate that.

I am not sure I could have taken over so much responsibility at many other firms. Not many firms would have allowed me to manage the complete investment process the way that Earlybird did.

Getting there.

Looking back on the last two and a half years that I spent with Hendrik, Christian, Max, Ciaran and Jason – and the whole back office team – things happened so quickly it is almost surreal. Not a single time did I go to work not being happy about what I am doing. Let’s face it, its a dream job in a city that is booming like no other in Europe. Perfect place perfect time. I consider myself to be super lucky to have worked among the guys and with the entrepreneurs I was allowed to support financially. With other peoples money. And that’s what we are doing as VCs. That is something I try to keep in mind all the time. Some people put trust in us that we do smart things with their money.

Overall, I worked with 8 founders and their respective companies.

I could write complete posts about how it was working with Valentin and Max from Number26 – having my most intense deal negotiations. Spending time on fairs with Fredrik from Enevo. Discussing open data with Javier and Miguel from CartoDB. Trying to understand the inner details of code repositories from Marcin from RhodeCode. Simply being stunned how illiterate I am every time I meet Bruce and Trent from ascribe. Seeing pure pashion for what he is doing every time I talk with Goran from Bonagora and Robert from Cashboard. And finally being stunned how Basti, Chris and Finn from Movinga can build a 300 people company in less than a year with revenue and margins other companies dream of after ten.

No post would do justice to the excitement I had in the last intense years meeting and working these guys. Thanks!

Love it. What’s next?

With Ciaran and Jason leaving Earlybird to run Blueyard, and Christian and Hendrik focussing on later stage deals, I was approached by a couple of funds in Europe about my new plans. I did not know I had any until that point. I was sure that Venture Capital is my passion and that the decision I made three years ago to make the move into this industry was a great one. And I was sure I wanted to continue work with early stage startups.

With Ciaran and Jason leaving Earlybird to run Blueyard, and Christian and Hendrik focussing on later stage deals, I was approached by a couple of funds in Europe about my new plans. I did not know I had any until that point. I was sure that Venture Capital is my passion and that the decision I made three years ago to make the move into this industry was a great one. And I was sure I wanted to continue work with early stage startups.

A common friend put me on the radar of the folks at Creandum, and I had followed them ever since I started in this industry. I was excited to learn that Creandum was expanding into Western Europe and was looking for someone to cover the German speaking market for them.

I decided to take on the next challenge and join a fantastic team of likeminded investors, entrepreneurs, data scientists and simply smart people to help build the next level European venture capital firm. Something I have been looking forward to for the last months. In February 2016 I will be joining Creandum.

And boy am I nervous and excited again! Very nervous. And very excited.

Also, my time in Berlin comes to a temporary end. My family and I will be moving to Stockholm for some time before we return to Berlin next year. I look forward to both. Stockholm is known in the tech scene for its design and product driven innovators. Sweden is known for its friendly people and beautiful nature. I want to enjoy all of it.

Hej Creandum.

The post Thank you and goodbye Earlybird appeared first on signed.vc.

]]>The post Everyone should benefit from the meeting – not just you appeared first on signed.vc.

]]>I am starting to reflect on how to become better in my job more and more. How do I make sure the people I interact with benefit the most from my work? That is foremost the entrepreneurs I work with and my partners. But there is one bigger group that I am focussing on more: everybody else I interact with.

I am starting to be more selective on who to spend time with (the struggle of having a good filter – this is a huge issue and most VCs I talk to). However, for those I do meet, I try to be a better sparring partner, someone who sometimes just listens and then makes the right introduction, someone who rather asks questions then telling opinions right away. I am trying to be less passive and suck information, but rather make sure the other person leaves the room – no matter the original intent – and remember it as time spent valuable.

About half a year ago I started developing this mantra, that I now try to follow in every meeting: How do I make sure that the other side of the table benefits from the meeting just as much as I do?

When I go over the documents I received, I already try to think of people that would benefit from meeting the other side even more than I would – both on the investor and on the biz dev side. And usually these are the people my meeting guest will benefit from, too.

Why? I fundamentally believe in the old saying: you always meet twice. Connecting people is a huge part of this industry, and when you connect people who benefit from meeting each other, they connect you with the people you want to meet. And everyone wins. Sounds obvious, but applying it to every single meeting (yeah, there are some where it doesn’t happen) has pushed me to becoming a better investor by a little.

On the other hand, by thinking about who knows about an industry better than I do, who could be a valuable customer, who could be a great future employee and who could help solve a certain problem – helps me understand the situation / model / industry / market better as well.

And so, everyone wins.

The post Everyone should benefit from the meeting – not just you appeared first on signed.vc.

]]>The post Example Seed Stage VC Pitch Deck appeared first on signed.vc.

]]>2 years into the industry, I meet great teams who build phenomenal products that one day might have substantial impact on society. However, in #Berlin, selling what you are doing can still be improved. The first cohort @Techstars Berlin demonstrated how to pitch your startup on another level. Impressive. This is new, and this is part of the game as well.

Unfortunately, not everyone is lucky enough to get pitch training and (from what I hear) animators and designers to build their pitch decks at Techstars. For those, I built a skeleton pitch deck to cover the basics. I have been sending this slide deck out maybe 20 or 30 times so far, whenever it was too early for us to invest for us but I felt the company could benefit from telling their story better. So far, the feedback was good so I decided to offer it to everyone.

Others have built great sample pitch decks to help early stage entrepreneurs before. This is my thought on the matter. Please take it with a grain of salt.

The post Example Seed Stage VC Pitch Deck appeared first on signed.vc.

]]>The post Banks are general supply shops from the 80s appeared first on signed.vc.

]]>

The issue of most major banks until today is that they follow a strategy of a very deep and a very wide value chain. That means, they offer a huge variety of products, which they handle from IT to after sales support. And everything in between. They run the core banking infrastructure, pre sales, the core product, and after sales.

The products range from retail banking, private banking & wealth management, products for external asset managers like tax advice and private label funds, to internal asset management and investment strategy and research products. Further, most banks offer corporate banking (split between SMEs and large caps), treasury, FX, brokerage, leasing & factoring, global finance and transaction banking, transportation, fixed income, equity and M&A. In addition, retail banking, credit, mortgages, all kinds of saving products, pension products, investment products – and payment. The list could be extended both vertically and horizontally.

In short: banks offer a huge variety of deeply integrated products.

This makes it is easy to cut of some edges and start a highly specialized business. This is what we see every week now. We call them FinTech startups.

Not only is it easy to leave out some services that banks still run in-house (scoring, KYC, IT) around their products. But banks also offer this service in pricy real estate locations. They call them bank branches. Most of us have not set foot in one lately.

This opens a broad flank for highly specialized companies to target one product only. Dissect the offering, add a modern IT infrastructure (cloud, mobile, analytics, prediction, big data, a revamped contract / KYC handling), and sell it cheaper than any account manager in a nice suite could do. Online.

This is what we see in the current FinTech boom.

The width of banks horizontal diversification and the depth of value creation of banks is still archaic. Few industries have managed to cope with this structure as long as banks. Most industries have trimmed down to their core business by now. When you try to do everything, you don’t do anything right. This has lead to the fact that most retail bank product offerings are interchangeable, as no one is really bad, but no one is really good either. That’s where the brand of a bank comes into play to convince customers to go with one or the other offering. And if in addition you have a huge capex underlying, competing on price gets difficult, too. As even most vertically specialized banks still operate a big amount of their vertical activities themselves, there is a big chunk of optimization potential for newcomers in the operations alone. We see this in the competition of classical direct banks with mobile banks for example.

Let’s face it, overall banks today still look and feel like general supply shop from the 80s.

The specialization and disruption which we have seen in other industries (e.g. travel, traditional retail, communications) now accelerates in financial services / banking. Things started to change ten years ago slowly, but the acceleration we see in Europe over the last three years is impressive.

That is not a problem by any means. We have seen this disruptive development in other industries already – where highly specialized players and services have shifted to become complementary partners. Add the degree of digital technologies and user adoption to them, and you can explain what is happening in FinTech today.

We as VCs are happy to see so much disruption in the industry. Not all FinTech startups will be successful, but one thing is sure: some will. And banks will struggle to justify their existing cost structure, and margin business. It will take time to disrupt the industry to the degree that we see others being chopped up and put together again.

However, what we see right now is a race into all verticals of banks.

And it would be beneficial for banks to realize, that this is 2015.

The post Banks are general supply shops from the 80s appeared first on signed.vc.

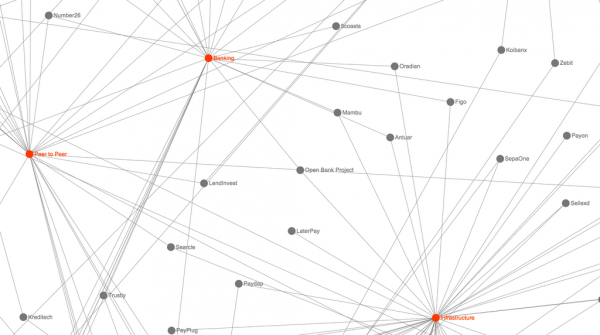

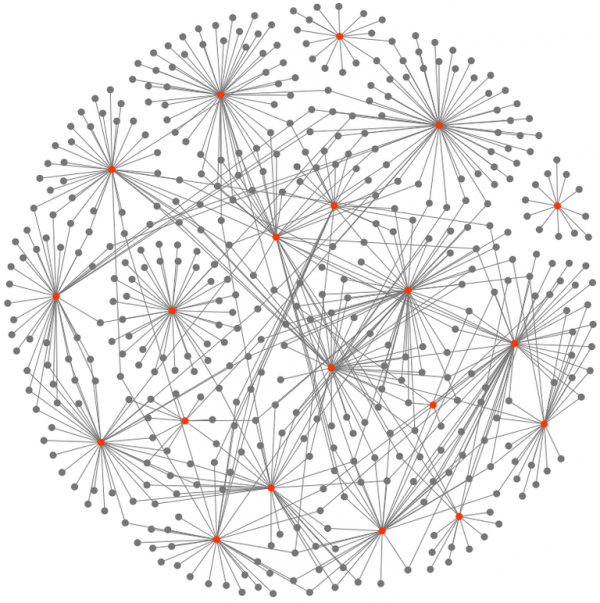

]]>The post Interactive map of the European FinTech landscape appeared first on signed.vc.

]]>To better understand the industry, we started mapping it. First we had lists. We soon realized that having a single dimensional list did not do justice. Our portfolio company number26.de for example does personal finance management within its retail bank account. And offers the functionality to send money easily from peer to peer. Hence it competes directly with peer to peer wallets. And with other personal finance management startups. Lists were difficult to maintain.

I then started to build mind maps. However, the end nodes of mind maps also only arch back to one category. So we had to duplicate startups and hook them to category nodes. Not very sexy.

Finally, I started to develop a view that I believe does justice to this multidimensional industry: a self sorting graph. Startups are hooked to the main categories they operate in. This allows to understand one category within FinTech, but also which startup competes with who.

The map is based on sigma.js (read this for more on this great JavaScript framework) and Force Atlas 2 (read this for the math behind it) – a graph layout algorithm on top of a JSON export fed by a MySQL database – I believe to now have found a great way of displaying the connection between the multiple startups within the European FinTech Industry.

Feel free to play around with it – please add startups that we missed – and give feedback to “schmincke at earlybird dot com”.

The post Interactive map of the European FinTech landscape appeared first on signed.vc.

]]>The post I will build an app store on top of it: On SaaS APIs appeared first on signed.vc.

]]>There is one thing that many new startups seem to be ok with, and I see a clear pattern to this: It is alright to share my users, as long as I own them.

For quite some time, monolithic software was built – shielding the user from anything and everyone. The model: Selling a license, and even building a SaaS platform that would grant permanent or temporary access to the software to each user that was attracted. Then came the REST API. Today, I would claim that 7 out of 10 companies I meet per week feature an API as the core element of their offering. Many of them not only grant access to data, but actually provide direct access to the customer.

It is fascinating to see that many models today even rely on outsourcing a big chunk of their value proposition to outsiders. And by outsiders I don’t necessarily only mean the crowd / community – but companies living of it. One used to call this “releasing unfinished software” – today it is called “opening feature seats to others” or “focussing on the core USPs”.

This leads to a mesh of software: dropbox / mailchimp / shipping providers / payment gateways / user-reactivation / SEO optimization / cross selling … the list seems endless. And all this is available everywhere.

But where does this lead to? How do offerings differentiate? If I can include the same service provider via an API (or App Store as it is called mostly) into any shopping software, into any blog software, into any SaaS platform in general – how do I differentiate? Well ultimately in the core offering – and in acquiring users the best possible way.

As a VC, I see great successful companies banking on this method. The more successful companies have already opened themselves to outsiders (even Microsoft seems to be doing it lately), actively improving the product offering through docking on through an API. However, “yeah, I will build an app store on top of it and then my business model makes sense” seems only intellectually intriguing. It does not make sense for everyone. And I believe the ones that understand that will be the winners of the next generation of SaaS companies.

I love how companies are now sharing users, enabling better products through APIs. We will see where this leads to, but I believe that understanding how to own and keep the user will become even more important in the future, where SaaS platforms can easily share a good part of the product USP by docking on the same external service providers.

The post I will build an app store on top of it: On SaaS APIs appeared first on signed.vc.

]]>The post The 18 verticals in the European FinTech Ecosystem appeared first on signed.vc.

]]>To give an overview, I want to group and classify the different types – I call them verticals though it might no be 100% correct – of financial technology startups. I can across examples of each of them, over the course of the last year.

This list is not exhaustive of course – but it should give a good feeling about what’s happening in Europe right now.

I. Payment

- Peer-to-Peer Payment

e.g. payments flowing in real life from one user to the other. Could be crypto currency, bank account to bank account, or wallet to wallet transaction. Either as a feature of a product or the standalone USP of an app. - Remittance

e.g. sending money abroad easily, cheap and often circumventing existing offline infrastructures. - B2B Payments

e.g. transaction of payments between businesses, or optimizing working capital for businesses, or factoring of invoices. - POS / Mobile Payment

e.g. enabling payments electronically, often mobile phone bases, often using Bluetooth, NFC or QR Scans mostly using dedicated wireless devices or parts of upgraded casher systems at the point of sales. Also tablets or smartphones that are used as a register via dedicated applications. Also hardware that is used to accept payments via e.g. credit cards. - Social Payment

e.g. applications that allow group paying, sharing of bills on premise, mobile or via social networks.

II. Infrastructure

- Processing / PSPs / Acquirers

e.g. infrastructure / SaaS models to server as a single payment gateway for clients who use this services facing end consumers, often offering multiple payments through one service. Also services which aggregate and analyze payment data, standalone or as value add. - Financial Networks

e.g. closed online circles providing members with semi exclusive content, data and network within certain financial circles like VC, PE, Hedge Funds and other investment classes. - Scoring

e.g. profiling users on public, semi private and behavioral data to derive a score, provided for others or to issue own credit. - Credit / Debit Card innovation

e.g. new forms of issuing, pooling or managing credit and/or debit cards. - Crypto Currency

e.g. applications that allow storage, mining, applying, transferring or converting of digital currencies.

III. Investment

- Lending (C2C, C2B and B2C)

e.g. management of many to many, few to many, many to few or crowd based lending based on currency or crypto currencies – often without involving a regular credit issuing institution. - Investment Strategy / Portfolio Management

e.g. allowing insights, or providing services to invest into (often mirroring) public, big data or crowd based investment strategies. Also web and mobile based asset management, often using more simple underlying financial products to provide easy money management for people without time and/or expertise. - Equity Financing / Funding / Secondary

e.g. enabling companies to raise funding for equity and/or products from mostly private investors. Also platforms that allow trading of equity on the secondary market. - Fx

e.g. trading or issuing of foreign currencies, real time price optimization or services around Fx settlement, standalone or integrated in ERP systems. - Financial Research and Data

e.g. market insights – often structured – for business and private users.

IV. Personal Finance

- Personal Finance Management

e.g. stand alone or integrated applications to manage, analyze and budget personal spending. Often include forecasting auto grouping of past behavior. - Wallets

e.g. stand alone or integrated applications to store and send money – mostly in real time. - Insurance

e.g. applications for brokers to manage customers, customers to manage insurances, comparing prices and or optimizing insurance situations.

Some categories have overlaps within groups – but this is the best way of clustering and categorizing in my eyes. Did I forget any groups or categories? Drop a comment and I will add it to the list.

The post The 18 verticals in the European FinTech Ecosystem appeared first on signed.vc.

]]>The post Why fintech? appeared first on signed.vc.

]]>First, fintech is hard. Fintech requires more than sourcing and selling. Smart SEM or customer acquisition tactics. It usually requires deep integration into the technology of partners, that often use legacy systems. And 600 page manuals. Nope, not everyone has a sexy REST Api in this world. Digging through these manuals, negotiation for adaptions to better ingrate ones service and convincing the slow moving world to allow to draw data or push some is time consuming, requires special skills and can be frustrating. And mastering difficult things is always rewarding. The results are difficult to copy and give a certain form of gratification that feels like beating a system, rather than only overcoming a difficult hurdle.

Second, fintech startups often work as enablers or as a platform for people. Or at least have an impact cross vertical, not only for a single case. They enable other companies to exist, scale or internationalize. Fintech startups enable people to pay easier, invest smarter, save time and resources that can be used otherwise. They often make your life better, rather than just serving a specific need.

Third, most startups I see have a good possibility to become unicorns or at least scale massively with little resources. And I don’t mean the upfront cost in tech. Which can be big. The leverage is unbeatable. Small teams can have a dramatic impact. If successful. Investors call this unlimited upside potential. There are enough examples which succeeded, or are on a good path getting there. And this is fascinating both for an investor and for someone who is interested in the business part of the newspaper in general.

And finally, the innovation we are going to see in the financial technology space in the next years is going to overcome borders, disrupt historicly existing systems, make ourselves wonder why things were socially accepted the way they were and ease our lives fundamentally. The best is yet to come.

The post Why fintech? appeared first on signed.vc.

]]>